- The Dutch economy is growing faster than expected

- Number of unemployed is increasing…

- … number of jobs too

- US inflation is a bit disappointing…

- … causing bond yields to rise

Google Translated from Dutch to English. Here is the link to the original article in Dutch. The article was originally published on 17 February 2023.

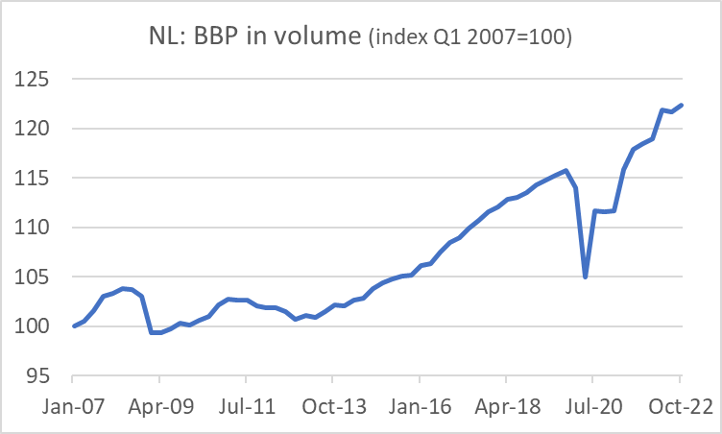

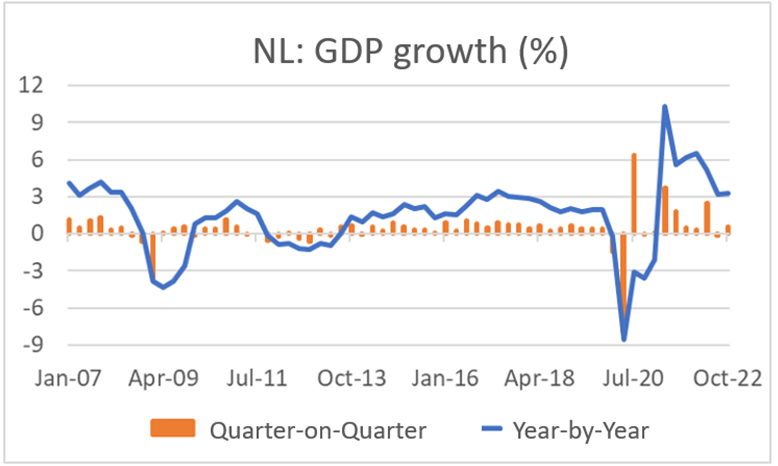

Dutch GDP grew unexpectedly fast in the fourth quarter: 0.6% compared to the third quarter and more than 3% compared to a year earlier. Total GDP (volume) in 2022 was 4.5% higher than in 2021. The first picture shows that our GDP is well above pre-pandemic levels and that we are also back on the trendline that emerged after the euro crisis manifested ten years ago.

Source: Macrobond

That growth in the fourth quarter was better than expected and would have been even higher if companies had not reduced their inventories. Economists had been much more frugal in their expectations. In hindsight maybe stupid. All Dutch households received 190 euros in November and December. What may have also played a role was that Christmas in 2021 was thoroughly ruined by the lockdown then set a week before Christmas. This time we were free. The consumption of services was therefore no less than 10.6% higher in the fourth quarter than in the fourth quarter of 2021.

Anyway, the consumer showed its best side especially in December and economists, with their too low growth forecasts for Q4, did not, or insufficiently, have this in mind. The volume of household consumption had been below the average for the third quarter in October and November, but a true spending spree in December lifted this volume to a level 9.9% higher than a year earlier. In the national accounts, private consumption growth in the fourth quarter therefore grew by 0.9% q-o-q and 3.7% y-o-y.

Source: Macrobond

If those two times 190 euros played an important role, then you have to fear a bit for the growth in the current quarter. On the other hand, the European gas price has fallen sharply and our exports, which already performed remarkably well in 2022, may benefit from the opening of China.

The Dutch labor market continues to surprise. Unemployment rose slightly in January: 3.6% compared to 3.5% in December. What is so surprising is that the participation rate in our country has risen sharply after the pandemic. In the US, the participation rate has fallen and they wonder why that is and why the participation rate is not rising now that there are so many vacancies. You would think that such a large number of vacancies would tempt people who are on the sidelines to enter the labor market. Not so in the US. Well with us. Because unemployment in our country may have risen in January, but so has employment. Compared to January 2022, the working population was about 3%, or 291,000 people, larger. I assume that this includes several tens of thousands of Ukrainians, but that aside. The number of workers increased by 284,000 over that period.

Disagreement between the Fed and financial markets

Inflation in the US was 0.5% mom and 6.4% y-o-y in January. That was slightly higher than expected. Core inflation was 0.4% mom and 5.6% y-o-y, also slightly higher than expected.

There is currently a major disagreement between the Federal Reserve and the financial markets. The Fed has been calling for some time that it will raise interest rates further and that thinking about interest rate cuts is out of the question. But financial market players have been pricing in a rate cut before the end of the year for some time.

However, the disappointing inflation figure led to slightly higher bond yields this week. Apparently, financial market players are starting to scratch their heads and consider whether the Fed might be right after all. Not completely convinced yet. The effective yield on 10-year government bonds is still much lower than on 2-year bonds.

Source: Macrobond

As I have argued many times before, US inflation is unlikely to fall very hard towards the Fed's 2% target as long as the rise in housing rents continues. And that is still the case. Rents weigh about a third in the US inflation basket. In January rents were 7.9% higher than a year ago. In the US, rent increases follow house prices with a lag. House prices have been falling for several months and that will certainly lead to a leveling off of rental inflation. If house prices continue to fall, rents will also fall in absolute terms. Then it can go fast in the right direction with inflation.

Source: Macrobond

U.S. manufacturing output rose 1.0% from December. That's a healthy number. Keep in mind that production fell by 1.8% in December. I think the weather here has caused some disruption. In December, large parts of the US were hit by severe winter weather and public life was disrupted. That undoubtedly dampened activity in December, making recovery easy in January. The year-on-year comparison still shows a minus: -1.3%. So it's not over yet.

Summarizing

This week's macro news has yielded little shock. The Dutch economy grew faster than expected in the fourth quarter of last year. Whether we can keep that up remains to be seen. The two times 190 euros has undoubtedly given a boost to spending and that will not be repeated. But foreign trade also contributed to growth, which may benefit in the coming period from the impetus that China's opening will give to world trade.

Inflation in the US was slightly disappointing in January and capital market interest rates subsequently rose slightly. You could say that the Fed has scored a point in the disagreement that the US central bank has had with the financial markets for some time. But the disagreement is not over yet.

.png)

.png)